REPORT OF THE

BOARD OF DIRECTORS - THE BOARD OF MANAGEMENT

BOARD OF DIRECTORS - THE BOARD OF MANAGEMENT

Pioneer in creating the Foundation

FINANCIAL STATEMENTS

Unit: VND billion

| Financial statements | 2022 | 2023 | |

|---|---|---|---|

| A | Financial statements | ||

| 1 | Total assets | 1,813,815 | 1,839,613 |

| 2 | Revenue | 114,592 | 135,614 |

| 3 | Tax paid in the period | 6,426 | 11,648 |

| 4 | Profit before tax | 37,368 | 41,244 |

5 | Profit after tax | 29,919 | 33,054 |

| B | Key financial indicators | ||

1 | Capital | ||

| 1.1 | Charter capital | 47,325 | 55,891 |

| 1.2 | Capital adequacy ratio | 9.95% | 11.39% |

| 2 | Business results | ||

| 2.1 | Deposits | 31,181,399 | 32,949,742 |

| 2.2 | Loans | 2,351,845 | 2,724,301 |

| 2.3 | Debt collection | 2,166,889 | 2,600,818 |

| 2.4 | Non-performing loans | 7,820 | 12,634 |

| 2.5 | Loans (including corporate bonds)/Total deposits in 1st market (in VND) | 91.12% | 90.46% |

| 2.6 | Loan to deposit ratio (LDR) in compliance with regulations of State Bank of Vietnam(*) | 73.90% | 77.90% |

| 2.7 | Non-performing loans/Total outstanding loans in 1st market | 0.68% | 0.99% |

| 3 | Liquidity(*) | ||

| 3.1 | Liquidity reserve ratio | 25.00% | 19.60% |

| 3.2 | Liquidity ratio within 30 days | ||

VND | 73.10% | 105.40% | |

Foreign currencies in USD equivalent | 96.30% | 82.10% | |

(*) Ratios calculated for individual data dated December 29th, 2023 according to the provisions of Circular No. 22/2019/TT-NHNN and as amended and supplemented

Total assets

Unit: VND billion

Unit: VND billion

1.42

%

%

1.42

%

%

Profit before tax

Unit: VND billion

Unit: VND billion

10.37

%

%

10.37

%

%

Revenue

Unit: VND billion

Unit: VND billion

18,35

%

%

18,35

%

%

SHARES

| Total shares | Type of shares | Number of transferable shares | Number of restricted shares |

|---|---|---|---|

| 5,589,091,262 | Ordinary shares | 569,843,260 | 5,019,248,002 |

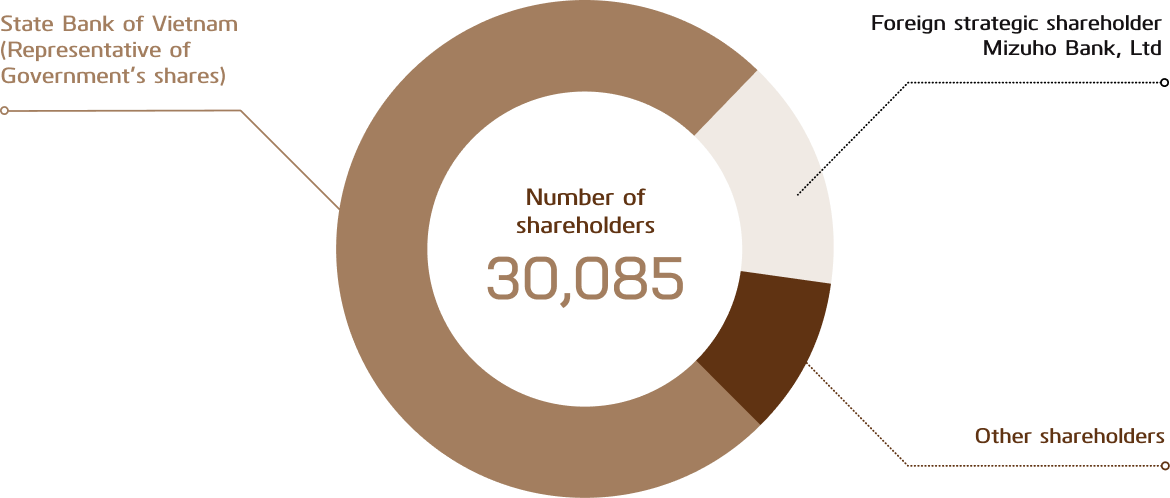

| No. | Name of shareholder | Total shares | Ownership rate | Number of shareholders |

|---|---|---|---|---|

| I | State Bank of Vietnam (Representative of Government’s shares) | 4,180,828,481 | 74.80% | 1 |

| II | Foreign strategic shareholder Mizuho Bank, Ltd | 838,372,264 | 15.00% | 1 |

| III | Other shareholders | 569,890,517 | 10.20% | 30,085 |

| 1 | Domestic individual shareholders | 40,094,837 | 0.71% | 28,308 |

| 2 | Domestic institutional shareholders | 62,808,938 | 1.12% | 166 |

| 3 | Foreign individual shareholders | 3,229,704 | 0.07% | 1,392 |

| 4 | Foreign institutional shareholders | 463,757,038 | 8.30% | 219 |

| Total | 5,589,091,262 | 100.00% | 30,087 |

INVESTMENT STATUS, PROJECT IMPLEMENTATION STATUS

Vietcombank Leasing Co., Ltd

VCBL

Profit before tax in 2023

15,332

VND billion

Vietcombank Securities Company, Ltd

VCBS

Profit before tax in 2023

607.57

VND billion

Vietnam Finance Company

VFC

Profit before tax in 2023

1.94

HKD million

Vietcombank Remittance Company

VCBR

Profit before tax in 2023

23.23

VND billion

Vietcombank Laos Limited

VCB LAOS

Profit before tax in 2023

26.75

LAK billion

VCB Money, Inc

VCBM

Profit before tax in 2023

767.79

$ thousand

Vietcombank Tower 198 Ltd

VCBT

Profit before tax in 2023

79.36

VND billion

Summary of joint ventures - associates’ performance and financial situation:

Vietcombank – Bonday – Ben Thanh Joint-venture Company Limited

VBB

Profit before tax in 2023

220.75

VND billion

Vietcombank Fund Management

VCBF

Profit before tax in 2023

81.35

VND billion

Vietcombank - Bonday Joint-venture Company Limited

VCBB

Profit before tax in 2023

51

VND billion

ASSESSMENT ON BUSINESS PERFORMANCE IN 2023

VIETCOMBANK’S BUSINESS PERFORMANCE RESULTS

Capital mobilization from market I reached

1,405,610

VND

Billion

Billion

up 11.8% compared to 2022

Credit balance reached

1,280,547

VND

Billion

Billion

up 10.8%compared to the end of 2022

Control debt quality in alight with set targets

Group 2 debt ratio was at

~0.43%

bad debt ratio was at

~0.99%

The ratio of provision for bad debts on the balance sheet reached

THE highest level

in the banking system.

The ratio of international payment & trade finance reached

19%

Payment increased by

24%

respectively compared to 2022

transaction volumes increased by

20.5%

respectively compared to 2022

The number of international credit/international debit card customers increased by

12%/102%

compared to 2022

Profit before tax

completed the plan assigned

by the SBV and the General Meeting of Shareholders in 2023.

ROAA and ROAE indexes remained high, At

ROAA

1.81%

ROAE

21.99%

VCB maintains its position as the leading

commercial bank in terms of quality and operational efficiency. It continues to be at the forefront of the banking industry and is one of the largest contributors to the national budget. VCB remains strong as a listed company with the largest market capitalization and is recognized among the top 100 listed banks with the largest market capitalization worldwide.

MANAGEMENT PERFORMANCE

REDUCTION OF INTEREST RATE BY

0.5%

/year

FOR ALL CUSTOMERS WITH EXISTING DEBIT BALANCES IN VND

ONE OF THE FIRST 6 BANKS

TO SUCCESSFULLY DEPLOY APPLE PAY

TO SUCCESSFULLY DEPLOY APPLE PAY

REDUCTION OF INTEREST RATE BY

0.5%

/year

FOR ALL CUSTOMERS WITH EXISTING DEBIT BALANCES IN VND

ONE OF THE FIRST 6 BANKS

TO SUCCESSFULLY DEPLOY APPLE PAY

TO SUCCESSFULLY DEPLOY APPLE PAY

To successfully implement the action guidelines of “Transformation, Efficiency, Sustainability” and achieve the results of thesix breakthroughs and three key business restructuring areas, the Executive Board has developed a consistent and decisive approach of “Responsibility - Determination - Innovation”. This approach has been integrated throughout the organization and enforced vigorously to address key management and operational priorities in 2023.

- Firmly directed to promote credit growth right from the beginning of 2023 while maintaining strict credit standards. The focus remained on managing credit expansion towards expanding industries and clients with strong financial capabilities and risk resilience.

- VCB took proactive and responsible measures to adjust and lower lending interest rates to support businesses in their production and business recovery. Right from the beginning of the year, VCB implemented a 0.5% annual interest rate reduction for all customers with existing VND-denominated debt throughout the year 2023. Additionally, VCB launched various programs to lower lending interest rates for disbursements made during the year, providing support to customers in their production and business recovery efforts.

- In the context of challenging credit growth, the capital sources were continuously adjusted to provide a basis for reducing lending interest rates and supporting customers.

- Completed Phase 2 of the RTOM project with 55 deliverable reports for three components: (i) new sales and customer service model at branches, (ii) customer segmentation policies, and (iii) new retail credit model.

- Implemented the RLOS system across the entire portfolio, covering 72 retail credit products.

- Being one of the first six banks and the only state-owned bank to successfully deploy Apple Pay in the Vietnamese market.

- Successfully launched the Vietcombank Visa Infinite card with outstanding privileges, offering customers unique experiences.

- Successfully deployed and operated the private placement corporate bond trading system, enhancing VCB’s image, brand, and benefits.

- Signed comprehensive cooperation agreements with corporations and conglomerates, providing holistic financial solutions and specialized services for wholesale banking and retail banking.

ORIENTATION OF BUSINESS OPERATION IN 2024

Some key indicators

Total assets up by

≥ 8%

COMPARED TO 2023

Deposits in 1st market

Deposits growth in line with credit growth

Credit

≥ 12%

and within the limit assigned by SBV

Non-performing loan ratio

< 1,5%

Profit before tax up by

5%

ASSESSMENT BY BOARD OF DIRECTORS

IN 2024, VCB WILL FOCUS ON 6BREAKTHROUGHS

1

DRASTICALLY DEPLOY THE STRATEGIC ORIENTATION TOWARD 2030

2

STRENGTHEN THE ORGANIZATION, IMPROVE THE QUALITY OF HUMAN RESOURCES

3

INNOVATE THE GROWTH MODEL ASSOCIATED WITH RESTRUCTURING OPERATIONS.

4

PROMOTE CUSTOMER CARE AND PRODUCT DEVELOPMENT

5

COMPLETE MECHANISMS AND POLICIES

6

DEPLOY SUCCESSFULLY THE PLAN ON MANDATORY TRANSFER OF A WEAK CREDIT INSTITUTION.

IN 2024, VCB WILL FOCUS ON 6BREAKTHROUGHS

1

DRASTICALLY DEPLOY THE STRATEGIC ORIENTATION TOWARD 2030

2

STRENGTHEN THE ORGANIZATION, IMPROVE THE QUALITY OF HUMAN RESOURCES

4

PROMOTE CUSTOMER CARE AND PRODUCT DEVELOPMENT

6

DEPLOY SUCCESSFULLY THE PLAN ON MANDATORY TRANSFER OF A WEAK CREDIT INSTITUTION.

5

COMPLETE MECHANISMS AND POLICIES

3

INNOVATE THE GROWTH MODEL ASSOCIATED WITH RESTRUCTURING OPERATIONS.

3 FOCUS IN BUSINESS RESTRUCTURING

1

Restructuring credit portfolio towards higher efficiency and sustainability, increasing the proportion and quality of collateral in total outstanding loans. Wholesale credit growth associated with customer and service development; Retail credit growth associated with gradual shifting in product structure to prioritize loans into manufacturing and business industries.

2

Strive to increase the proportion of service revenue. Increase services through digital channels and improve service quality and customer experience.

3

Increase the efficiency of capital management; optimize long-term capital investment portfolio, organize divestment and new investment to ensure sustainability and efficiency. Strongly develop VCB’s market making position.